In the past few years, the number of residents opting to live in secondary and tertiary markets has increased significantly. This migration to once less attractive markets has been driven by affordability, the opportunity for growth, and increased residential mobility. So, it’s not surprising to see that these smaller markets are on track to outgrow many major US cities. The increased level of competition and the exorbitantly high cost of entry in primary markets, along with the declining demand for CBD office space due to the Work From Home phenomenon, has driven investors to seek opportunities for profit elsewhere. In this article, we’ll discuss some of the up-and-coming secondary and tertiary markets to look out for in 2023 and the availability of capital for different property types in those markets.

Secondary markets, like Denver, Austin, and Portland, have seen significant population growth and job market expansion creating a need for more housing and amenities. Because these markets have less economic activity and exposure as primary markets, they aren’t nearly as saturated providing ample opportunity for investors. Tertiary markets, such as Charleston, Richmond, and Colorado Springs are not drastically different from secondary markets although they are usually more spread out and have smaller populations.(1)

There is huge investment potential in these growing markets for reasons such as less competition, lower barriers to entry, stronger growth potential, and a potential for higher returns. Over the next decade, members of the workforce and large companies will continue to move into these markets, creating an opportunity for investors to capitalize on more attractive acquisition economics. By entering these markets in the early growth stages, sponsors will be able to take advantage and in turn, see outsized returns on their investments.

Lenders used to be weary of these markets because of the inherent risk of investing in a smaller market with less demand and therefore reduced opportunity to push rents. Debt was more expensive for investors, and they also faced lower available leverage because banks needed to hedge for the riskier investment. Lenders are now keying in on these markets because of the larger demographic trends at play. People are choosing to live and work in less expensive cities as larger companies such as Microsoft, Google, and Coca-Cola move in.(2)

The lower level of competition is based on the fact that real estate private equity firms and big REITs generally focus on primary markets and sometimes secondary, creating fierce competition among themselves. This is driving up pricing and reducing cap rates. On the flip side, secondary and tertiary markets tend to be less popular among big investors and more accessible to all investors, lowering the level of competition and barrier to entry.

We’re seeing a greater focus on specific markets from both the debt and equity providers and therefore make sure we capture as much data as possible as these parameters change. Because of our hyper attention to detail, we’ll only approach the capital providers we know are interested in your target markets.

Implementation of Environmental, Social, and Governance (ESG) criteria within Real Estate investment plans is on the rise. According to CBRE’s 2021 Global Investor Intentions Survey, 60% of the survey respondents have implemented ESG metrics within their investment criteria, a significant increase compared to previous years(1). With the amplified focus on social responsibility, how can you be the next to implement ESG criteria within your investment platform and take advantage of this important trend in Real Estate investing? Socially conscious investors continue to adopt these standards, implementing them in their companies and overall investment philosophies allowing them to achieve attractive returns for investors while creating a positive impact on the environment and community.

Climate Change and its associated impact on our planet are one of the most pressing issues our society faces today. As we move towards a more sustainable future, real estate professionals can take the next step to reduce the negative environmental impacts of their properties. Some of these negative environmental impacts reveal themselves within the construction process and the yearly carbon footprint buildings produce with ongoing operations. To mitigate these negative environmental impacts, developers can incorporate water conservation methods, safe disposal of waste, and the use of renewable energy. One way this is measured in new builds is through the Leed Certification. Getting a property Leed Certified allows a landlord to implement a Green premium on rent while also reaping the benefits of numerous financing incentives. For example, HUD loans have a reduced mortgage insurance premium for green properties. Implementing these features would allow real estate operators to both increase profit and help reduce their burden on the environment.

As a society, recently we have been making major strides in equality, diversity, and other social measures to move towards a more just society. The “S” portion of ESG encourages business owners, managers, and real estate operators to consider the social impacts of their projects. Some examples are the impacts a business or investment has on the local community, a company’s employees, and the suppliers they partner with. Essentially, the goal of this metric is to ensure all of the stakeholders related to a business or project are treated ethically and fairly. To incorporate the social aspect of ESG into one’s investment strategy, investors should take into consideration the impact of a real estate project on the local community. Considering the local community, the lack of affordable housing is a major issue throughout our country. Local tenants are being priced out, and this is being exacerbated by the increase in new development projects and premium rents. Operators can also improve their social impact by focusing on the treatment of their employees by paying reasonable wages, offering various benefits, and encouraging the personal development of employees. One of the most important ways a real estate owner/developer can improve their social impact is by ensuring that the raw materials used in the construction or rehab process are being ethically sourced.

The final aspect of ESG is governance which focuses on how a company or real estate project is governed. Within a business, governance can be in the form of transparency, allowing shareholders voting rights on important issues, or ensuring board members do not have conflicts of interest. Particularly in real estate, firms have been working on improving the diversity of their board of directors and implementing corporate socially responsible policies. Real estate firms have also been adopting new technologies such as benchmarking and reporting platforms to ensure they are meeting their goals in terms of ESG metrics.

In recent years, firms have been working towards aligning their projects in accordance with ESG criteria. Operators have been focusing on incorporating environmentally friendly materials into real estate projects and improving social and governance aspects within their firms. Our society continues to further increase its focus on the implementation of ESG as sustainability and equality for all have become more important for employees and investors of companies. One reason why investors have been hesitant to invest in environmentally friendly building elements is due to the misconception that investing in ESG will reduce profits. As firms focus on environmental sustainability, this thesis is changing as they are finding that implementation of ESG criteria can help increase profitability.

As the industry continues to align itself with the ESG metrics, real estate firms will focus on implementing ESG criteria within their firm and investments. Investment teams are focusing on improving their green metrics within projects by working towards achieving certain certifications such as the Leed certification. The U.S Green Building council is responsible for reviewing projects and then certifying them with the Leadership in Energy and Environmental Design (Leed) Certification. Leed Certification is an internationally recognized green building rating system (2). There are different levels of LEED certification, depending on what sustainability and environmental aspects are implemented in a project will determine the level of LEED certification a project receives. As buildings achieve LEED certification, operators can both improve the lives of the people using the buildings and also charge a green rental premium to their tenants(3). As different elements are implemented to achieve the certification, projects will help reduce carbon emissions, improve environmental quality inside projects, create healthier spaces, and bring in happier tenants. Once owners implement ESG improvements to their projects, owners will be able to charge a green rental premium to their tenants. Green leases will incentivize owners and lessees to maintain certain usage metrics such as electricity per occupant (kilowatt hours per employee), water used by area, and the volume of waste disposed of in landfills as a percentage of total waste produced. With lease structures promoting change, we will start to see an increasing difference in prices between green rental premiums and brown rental discounts for projects.

For the social aspect of ESG, investors seek to implement socially beneficial measures. In the market, we are seeing an increase in affordable housing projects as we see sky-high rent prices. Building owners will also implement health and wellness amenities for their tenants to use. Especially with the recent coronavirus, we are seeing an increased emphasis on improved hygiene measures in buildings. In office space, owners are starting to redesign each of the spaces to promote the health of their tenants with improved air circulation systems and social distancing measures. Mixed-Use, multifamily, and retail owners are working to improve the tenant mix by including more healthy food options as part of their restaurant options. Governing bodies also will work to improve the diversity of their board of directors or executives and improve the tracking of their benchmarks with the increasing use of technology.

Previously the industry did not focus on ESG investing metrics. Lenders and investors did not place an immense emphasis on sustainability, social, or governance factors while looking at projects(4). As of late, investors and lenders have been working on implementing ESG criteria within their own companies, and have been placing more of an emphasis on this space within their investments. As capital continues the implementation of ESG metrics within their work, we will see capital providers creating invectives for ESG-friendly projects. For example, lenders will provide lower interest rates for projects that fulfill certain ESG criteria, leading to the incentivization of investment into a more socially responsible future.

Here at Lever, we have extensive knowledge and experience with a wide variety of lenders. Understanding how Debt and Equity partners are adjusting their criteria to incorporate ESG into their investing strategies, we see where the future is going with the incorporation of ESG into real estate. We can help advise you on the needs and wants of capital partners to help you strategically position your investment to achieve the most favorable capital terms to help support your project. As we see the prevalence of ESG investing in the Real Estate space, many capital providers are adjusting their parameters to incorporate ESG within their companies. Increasing the focus of a project to fit ESG goals, can not only help the investors but improve and grow the local community of investment projects.

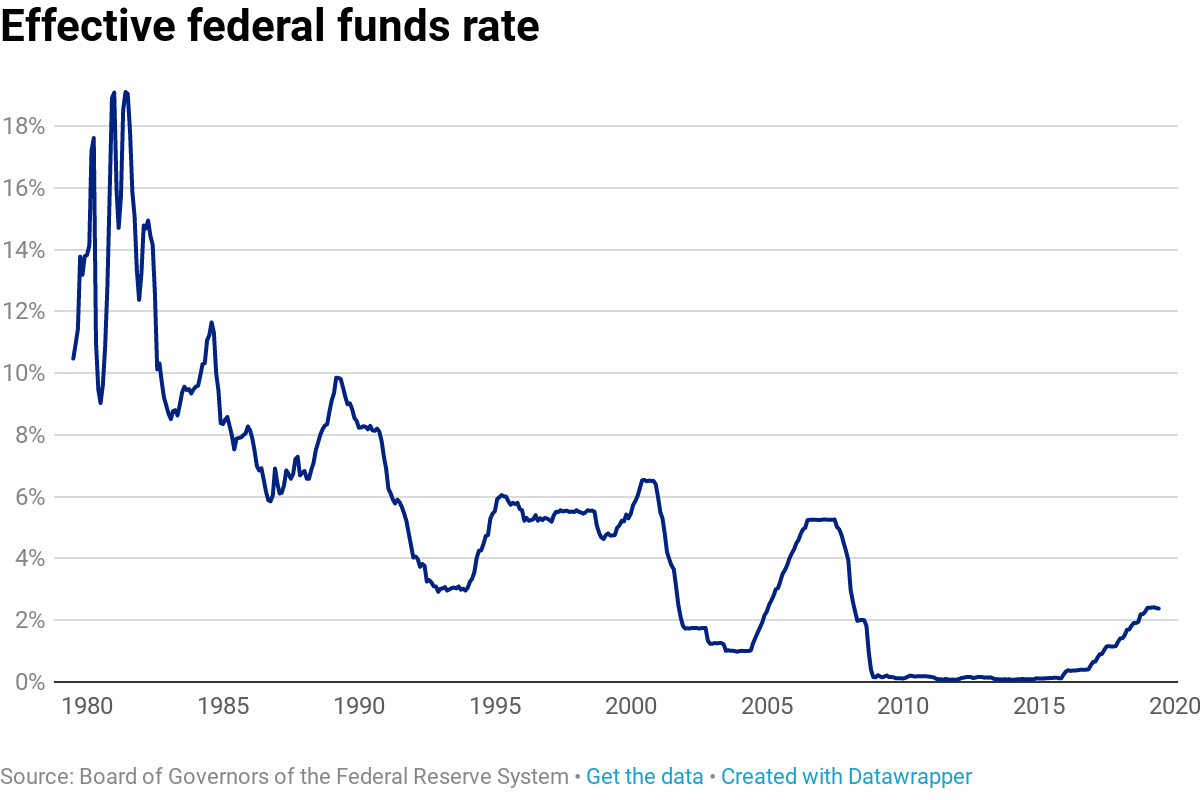

2022 will be a transformative era for capital markets in all sectors of the U.S. economy. In order to combat inflation caused by the stimulus measures implemented by the Federal Reserve during the COVID-19 pandemic, the Federal Reserve has recently decided to accelerate plans to increase interest rates. On December 15th, 2021, the Federal Reserve announced that it would end its pandemic-era bond purchases in March of 2022 and plan for three 25 basis point interest rate hikes by the end of 2022.

Due to the leveraged nature of commercial real estate, the rate hike by the Federal Reserve will have significant impacts on both debt and equity markets. As properties are often financed with commercial mortgages, commercial real estate markets are most exposed to interest rate alterations. With the rise in interest rates, we see the cost of debt rising accordingly. There are many debates regarding whether there will be increases or decreases in cap rates as a result of the interest rate increase and current macroeconomic factors.

Fundamentally speaking, increased interest rates lead to more expensive financing. From an equity perspective, acquiring new properties will have narrower margins, and in turn, may create a more conservative market. From a debt perspective, the increased rates may cause a decline in deal flow, however that loss in volume may be balanced by increased margins on invested capital.

The record low federal fund rate at the beginning of the pandemic (0% to 0.25%) reduced the cost of financing, and as a result, instigated a surge in buy-side activity, development, and increased prices. As with any artificial injection of capital to stimulate the economy, there are repercussions; one of which being the rapid increase in inflation. Thus the Federal Reserve’s upcoming move to not only increase interest rates but to raise them ahead of schedule has been a long time coming.

To look at lasting effects on commercial real estate markets, lenders and investors are looking towards two factors regarding interest rates. One, the effect of the interest rate hikes on cap rates, and two, the adaptability of commercial debt markets in regards to a rate hike. Concerning cap rates, there are generally two ways they can move. One, many believe that a rise in interest rates correlates with a rise in cap rates as property values decrease. Two, others believe that with increased interest rates, investors pay more to borrow capital, cutting into profits, and thus decreasing cap rates. However, when considering cap rate movement in relation to interest rates, we must consider a longer timeframe. As a result, it becomes hard to predict changes in cap rates as a result of increased interest rates, as other factors come into play such as capital flows, investor sentiment, and real estate fundamentals. Historically, changes in federal interest rates have not resulted in immediate changes in cap rates. The ultimate question is whether the market is well prepared to adapt to such a change.

Broadly speaking, the effects of rising interest rates are unpredictable. In addition, recent geopolitical developments such as the Russia-Ukraine War make it uncertain where the Fed will go with interest rates. However, we are certain that they will go up, and as such, create an environment for the movement of cap rates and the exacerbation of current squeezes on markets.

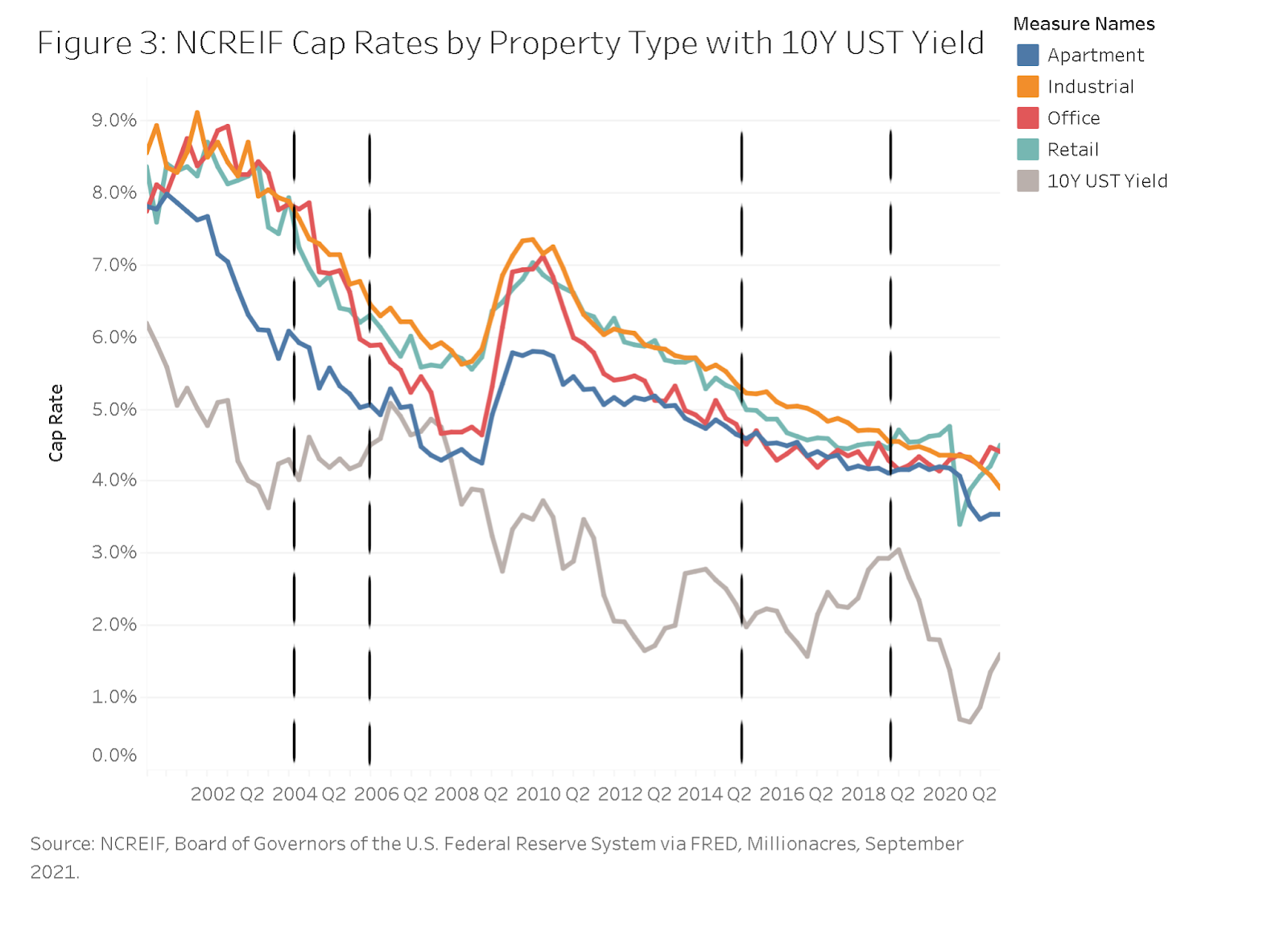

Graph 1.1

Graph 1.2

Secondly, we will see some asset classes take the hit worse than others. From the graphs above, we can see how historically speaking, with previous interest rate increases in 2015-2018 and 2004-2005, cap rates have generally compressed. However, stable cash-flowing asset classes with high occupancy rates such as multifamily will fare better than higher risk higher reward asset classes such as industrial, office, and retail. Since the margins on rent from these asset classes become tighter through the increase in interest rates, the risk of industrial, office and retail in regards to defaults will increase. We can see this through Graph 1.2, where apartment cap rates saw less compression than industrial, office, and retail asset classes. While the previous two interest rate hikes have led to cap rate compression, this is not indicative of what will occur in the present day. However, we do see that multifamily generally can withstand these macroeconomic trends better than office, industrial, and retail asset classes.

With the increase in the cost of financing, we will see spreads tighten as value add opportunities diminish. Since the market for many stable cash-flowing asset classes such as multifamily are already facing extreme demand and competition, the increasing cost of debt due to interest rate hikes will continue to chip away at the returns of value-add opportunities. According to Forbes, many investors in 2020 faced a difficult decision of either accepting lower returns with the appropriate amount of risk or finding ways to add more value to hit more opportunistic returns. The interest rate hikes of 2022 will exacerbate this trend as financing becomes more expensive. Ultimately, the interest rate hike will make competitive markets less viable, pushing investors to do two things. One, more conservative strategies such as core and core-plus will be adopted in order to accommodate for the increasing competitiveness of value-add opportunities, and two, we will see expansion towards suburban areas. Regions such as many of the Sun Belt states (i.e. Texas, North and South Carolina, and Florida) have high suburban demand for multifamily. According to Matthews Real Estate Investment Services, the demand in this region is driven by rapid population growth and increasing employment opportunities. With these growth and demand drivers, investors are looking to those areas to find more lucrative value-add opportunities.

According to Cushman and Wakefield, in the long term, this rate increase will benefit the health of property markets. The purpose is ultimately to reduce the potential for inflation to become entrenched, giving way to a more aggressive hike in the future, and potentially causing a recession. In the short term, interest rates are not necessarily a shift away from the current norm, but a force that can exaggerate many of the effects we saw in recent years. Multifamily will continue to offer stable returns, despite its slow yet steady cap rate compression, and investors will become more risk-averse and/or find opportunities in emerging markets.

In a constantly changing market, one slow step could be a missed opportunity. At Lever Capital Partners, our steadfast team of industry experts track the latest trends and understand how to source and utilize the best available capital. Whether you are looking for an equity partner, a lender, or a combination to fund your next project, Lever can advise you on obtaining the most attractive financing the market has to offer. Here at Lever Capital Partners, we pride ourselves on our wide range of experience in refinancing, recapitalizing, converting assets, ground-up construction, acquisitions, and our overall creativity in getting our clients the capital they need for any commercial real estate related transaction. Our industry professionals look forward to speaking with you about your next project.

The effects of COVID-19 have been felt throughout the entire commercial real estate sphere and continue to impact investment decisions across all property types. The pandemic has revealed a plethora of new opportunities in the marketplace, creating trends that are expected to continue into the foreseeable future. One of the most notable trends we are seeing is an uptick in multifamily investment and financing. The combination of record-high rental rates, surging demand, and skyrocketing market values is creating financing and capital event opportunities for property owners while forcing developers and investors to get creative.

Demand for multifamily housing has spiked dramatically in the first three quarters of the year and according to data from property management and analytics platform RealPage, “absorption of multifamily units jumped by more than 255,000 in the third quarter.” This extreme increase in demand can partially be attributed to the post-pandemic job market recovery we’ve been seeing, specifically regarding middle and higher-income jobs. Peter Linneman, of Linneman Associates, “believes that 3.5 million people will return to the workforce in the next six to nine months, and there will be an additional 2 million or more jobs added as the economy continues to grow” (Linneman, BisNow). Subsequently, more people than ever before can afford apartments due to stabilizing incomes related to job market recovery. This can be attributed to “the most recent ADP data from September [2021], indicating a [growth in] jobs [from] the previous two months”, due to the “elimination of the additional unemployment benefits issued in response to the pandemic” (Linneman, BisNow). Significantly more people are seeking employment as covid subsides and there is no shortage of available jobs, from the restaurant business to middle-income level jobs.

Additionally, the average price for multifamily assets has increased over the last 2 years, along with demand. Pricing and demand are projected to continue this upward trend in both the short and long term. In August of last year alone, there were “new construction permits totaling over 57,000 units issued across the U.S.” for multifamily development. This is the highest demand for permits in a single month since June of 2015. The trend is not expected to slow anytime soon, as 450,000 multifamily units are projected to be developed in 2023-2024.

While the demand for multifamily continues to surge as the market recovers from the pandemic, increasing uncertainty around office and retail assets has prompted many to convert those existing buildings. Both office and retail assets have seen record low occupancy rates during the pandemic. As a result, we are seeing many of the distressed properties getting converted to multifamily. This conversion strategy allows investors to capitalize on rising rents and demand in the multifamily sector, without having to buy in at the price levels we are seeing in the residential market. This trend has created a significant opportunity for developers and investors, as “renovations could cost about 30% to 40% less than new construction for the same number of units.” Not only are investors saving on construction costs, but they are also able to buy these distressed buildings at significantly lower prices than comparable existing multifamily properties in the same markets. Multifamily developers have experienced many challenges throughout the pandemic, especially regarding construction costs. These challenges and specifically the increased costs have made it difficult for individuals to start investing in the multifamily space, making the conversion strategy that much more attractive.

While multifamily investors key in on the conversion of commercial assets to multifamily given current market conditions and compressing cap rates, current property owners are able to take advantage by capitalizing on the current borrower/sponsor-friendly state of the capital markets. As cap rates compress, property owners/sponsors can get significantly more attractive debt, whether it be construction, bridge, Mezz, or permanent financing. “Multifamily cap-rate compression averaged 31 basis points in infill markets and 41 basis points in suburban markets” (ADG Multifamily). With market prices at all-time highs and the gradual increase we’ve seen in rental revenue due to record demand, it is the optimal time to get financing for a new project, refinance your existing debt, or recapitalize your equity. Investors have significant dry powder ready to be deployed in the multifamily space, whether it be a conversion or ground-up development. Meanwhile, banks, debt funds, and insurance companies aggressively look to deploy capital in both areas at rates lower than any other asset class.

Lever Capital Partners has significant experience in the multifamily space and can assist you in securing any financing needs for your next project. Whether you own an existing multifamily property and are looking to refinance or recapitalize, or you are a developer looking for construction financing for asset conversion or ground-up development, we have the resources and experience to get you what you need. We pride ourselves in our ability to bring clients a range of financing options that reflect only the best that the market has to offer.

Lever Capital Partners is speaking with lenders and investors on a daily basis and have been hearing that changes in underwriting are at the forefront of their minds. The number one question capital providers are asking is, “In the current post-Covid world, what changes have you made in your underwriting assumptions?”. The conversation is a non-starter if the sponsor has not thoroughly thought through these changes and can’t clearly point to adjustments made in the proforma with a compelling story to back it up. Here are a few of the major underwriting changes we’re requesting from our sponsors (for now) and our recommendations about how to present them to the market:

Cap Rates – Needless to say there is pricing uncertainty in the market (investment sales volume has dropped roughly 70% in Q2 2020 from the same period in 2019, according to CoStar and RCA Data). Pre-Covid comps are being ignored so it’s important to factor in a conservative premium to appease investors. Recently, we’ve seen value adjustments of 10%+ for multifamily properties up to 30%+ for hospitality, depending on the specific asset. Don’t be shocked when looking at your updated IRRs.

Rent Growth – Underwriting future income streams poses a considerable challenge for most properties without long term leases or credit tenants in-place. Across the board, investors are underwriting untrended rents and factoring in zero rent growth for the next 2-3 years. In rare instances, some markets are projected to have a negative rent growth rate over the next 1-2 years. Where you build / purchase will be heavily scrutinized now.

Exit Cap to Yield on Cost – In regular times we’d typically look for untrended yield on cost spreads of 150 basis points compared to the exit cap rate. The industrial and core multifamily spreads are holding close to those numbers but we’re seeing a much wider spread for all other asset classes. Be prepared to show numbers in the 175-200+ range.

Spec Development – Building spec has always been a challenge, even in the most bullish of times. Office and retail have required a fair amount of pre-leasing even in the early part of this year. But now, given the circumstances, nothing is going to happen unless you are heavily pre-leased with credit tenants in tow. Walking into the lender’s office with a mask and a dream won’t cut it, so start lining up those credit tenants.

Debt Assumptions – The lending world has dried up considerably with some participants leaving the market (debt funds) and others on the sidelines only willing to lend to existing relationships (banks). Overall, leverage has decreased with developments maxing out at 65% and more commonly in the 50-60% range while interest rates spreads have widened, increasing all-in rates. You’re likely going to need more cash, and investors are much more focused on the debt status than ever before.

Without these adjustments, most lenders / investors will take a quick pass. Your ability to identify and edit your original underwriting shows you’re adapting to the new normal, have an understanding of what metrics had to change and are able to craft a workable solution around the modified numbers. To come off as a sharp sponsor and on top of the market, we recommend having your changes ready to present by (1) preparing a doc that outlines your changes that you can share with investors and lenders and (2) crafting a compelling story for the asset and market that you can talk through.

These are the first things we ask for when looking at new deal packages. If you follow the above rules you might be one of the fortunate few to get a new loan or investor equity. We can help when you’re ready to “turn and face the strange” as Bowie said. We’re home working in our PJs waiting for you to call.

Investor appetite is lessening in 2019, according to firms surveyed for the 2019 Annual Investor Intentions Survey by CBRE. Of those surveyed, 98% intend to continue making acquisitions in 2019, but anticipate that they will do so at a slower pace. Furthermore, they are increasingly looking to secondary markets as well as alternative asset classes for yield. Amongst investors, the majority of investments are being made in pursuit of a stable income stream, followed by expectations of capital appreciation. This makes sense as prices across asset classes and markets are at or near all time highs.

Amongst investors, there is continued fear that 2019 may be the year of a global economic downturn. As we are all aware, this fear has been a growing concern over the past few years, but there has yet to be any strong indication that the apocalypse is now. Secondary to this concern is fear over what rising interest rates will do to the economy. At this time, the Fed seems to have indicated that they are taking a break from raising rates, so this fear, at least for 2019, can be put to bed.

Atlanta, Denver and Central Texas markets have emerged as leading metropolitan areas for real estate investment in 2019. Amongst Tier I cities, Boston and Chicago remain in favor while New York, Seattle and D.C. fall behind other Tier II and Tier III locations, including Las Vegas. These trends are continuations of what Lever Capital Partners has seen over the past few years and expects to continue to see moving forward.

Across asset types, industrial reigns top amongst investors. This continues a duel between industrial and multifamily spanning several years now. As tech giants continue to develop distribution plans for our increasingly e-economy, large investors have indicated they believe this sector is ripe with opportunity. Across asset types, value-add strategies remain most popular amongst investors, a trend that has now been increasing for nearly half a decade which Lever Capital Partners expects to continue in the short term. To the surprise of many, retail continues to hold its ground as an investment class, despite much buzz about the so-called “death of retail”.

Looking to the year ahead, the study indicates that 2019 is forecasted to be a slower version of 2018. Many of the concerns of the market have been sustained for several years now and trends in favorable real estate classes, investment strategies, and geographies are continuations from what Lever Capital Partners has seen in the past. In our experience over 2018, we saw increased activity in the senior housing, student housing, and industrial sectors. We anticipate these trends to continue as we move further into 2019.

At Lever Capital Partners we work closely with developers and owners to connect their projects with capital appropriate to their needs. We appreciate and anticipate the challenges the market cycle can bring to real estate transactions. We pride ourselves on our ability to have open conversations with clients and provide quick feedback, as to the market appetite, for their bespoke products. When partnering with developer clients in early stages, we are able to provide our market forecasts and help guide clients toward more financially feasible transactions.

By Adam Vanlerberghe, Managing Director, Lever Capital Partners

The topic of high construction costs has been popular over the last year and continues to be relevant into the new year. At Lever Capital Partners (“LCP”), we work closely alongside our Developer clients who must navigate and mitigate increased labor rates, material costs and labor shortages and delays.

The pain has been felt throughout the industry and especially within the Multi-Family sector where there remains a shortage of specialized trades needed to finish jobs. “We’re measuring an average delay of around five months,” says Andrew Rybczynski, senior consultant for CoStar Group Portfolio Strategy.

These delays can also lead to increased financing costs and liabilities to the Developer and/or Loan Guarantor(s). Delays lengthen the construction phase of a project, which typically carries a higher interest rate than the completed, income producing phase/product. Even worse, the delay could result in a loan default and/or costly loan extension fees.

At LCP, we anticipate and understand the challenges associated with developing a commercial project in today’s high-cost, often-delayed construction environment. We have realistic, open conversations with our Clients and help negotiate favorable loan terms, extensions and language to address such contingencies with our vast network of capital providers. Further, we will assist and advise our Clients on the preparation of budgets and proformas that account for these contingencies. When done properly, our Client and their project gain valuable credibility with capital providers, improving the likelihood of effectively closing the transaction.

By Amnon Cohen, Managing Director, Lever Capital Partners

Opportunity zones are areas designated by local governments that offer tax breaks under a new federal program. Investment firms have started to set up funds to distribute money specifically into these opportunity zones. There is a catch, every property within a qualified opportunity zone will not receive the same benefits.

There are multiple factors for investors to consider when it comes to investing money into opportunity zone properties. A few of these factors are, “the likelihood of getting a solid return on investment, the ability to quickly navigate the project approval process and the other programs that can be utilized alongside the opportunity zone benefit” (Banister).

“The industry was awaiting specific regulations from the Treasury Department, but experts believe it will allow investors to see significant increases in returns while also benefiting communities that otherwise might not attract as much investment. Develop founder Steve Glickman, who helped write the Opportunity Zone program while at the Economic Innovation Group, said the vision was to foster investment in low-income communities. But it was also important for local governments to select areas that could support private investment and create returns, and he said they did a good job of that. The census tracts selected cover 10% of the U.S. population, roughly 35 million people, and have an average poverty rate of about 30%” (Banister).

Here are the specifics:

-Gains can be reinvested into opportunity zones. If the project is held for longer than 5 years, 10% of the gains tax will be reduced

-If the project is held for 7 years 15% of the previous gains tax will be reduced

-If the project is held 10 years the any gains tax on the existing phttps://levercp.com/wp-admin/edit.php?post_type=news_2roject will be eliminated

-Among the answers provided, the Treasury Department said that a business can qualify as being in an Opportunity Zone as long as 70% of its property is in the designated area.

-Another important data point: Investors have 180 days from the sale of their stock or business to put the proceeds in an opportunity fund.

-Businesses also get 30 months to hold working capital for an investment in the Opportunity Zone, just so long as there is specific plan for a project.

At Lever Capital Partners we are also seeing positive ADR and Occupancy growth for most of our hotel clients. Given the run up in RevPAR, there has been a slew of development and the commercial real estate financing world is now taking a harder look at new development projects. Commercial real estate lending for new hotels is now only provided for the best owners where the STR report shows a true need for the asset in question. There’s been a bunch of CRE News about Airbnb and the effect that it’s having in the hospitality market but I haven’t seen it given the deals we’ve looked at. Maybe it’s having a greater effect in primary markets like NYC and San Francisco but many of the assets we’ve financed recently continue to have positive RevPAR trends. Overall we continue to like the hospitality segment but are cautious along with the lenders about what might happen if there’s a slowdown in the segment given the increase in average interest rate for commercial real estate loans.

– Adam Horowitz, Principal of Lever Capital Partners and President of the Real Estate Capital Alliance

I like Antonio’s article and hope that more family offices invest in multifamily assets. We’ve always enjoyed finding commercial real estate financing for family offices, but the challenge has been the locations. Antonio suggests that they should look in secondary and tertiary markets but what we’ve found is that the family offices tend to start off investing in locations near their home base with a GP partner before heading into a smaller market which makes it more difficult. We’d love to see more commercial real estate news saying that family offices are pouring into the space but only time will tell if they want to pick up multifamily assets and commercial building loans in markets they don’t know well.

– Adam Horowitz, Principal of Lever Capital Partners and President of the Real Estate Capital Alliance