The Millennial Influence: What the Rise of Short-Term Rentals means for the Housing Landscape

by: Ao Ma

The rise of the Millennial generation has had a significant impact on the real estate market, particularly in the area of short-term rentals. Reaching “peak Millennial” in 2015, USC Professor Dowell Myers states that the majority of this cohort has surpassed the age of 25, which has historically been the threshold for generations entering the first stage of the housing life cycle – homeownership.(1) For millennials, however, they arrived at an inopportune time. From 2014 to 2022, US multifamily rents have increased by a staggering 49%, while wages and salaries at private companies rose only 29.1%. High living costs, coupled with elevated student debt balances, have made it difficult for many Millennials to afford to buy a home. On top of this, Millennial values also gravitate toward short-term living solutions since they offer a more flexible lifestyle than traditional year-long lease terms, granting them very sought-after lifestyles to travel and “live in the moment.” As a result, the vast Millennial cohort has turned to short-term rentals.(2)

Accompanied by the rise in demand, data from AirDNA, a vacation rental analysis company, illustrates that the supply for US short-term rentals has increased by nearly 20% since 2019. Companies like Sonder, a boutique apartment-hotel hospitality company, have expanded their short-term rental offerings by operating traditional condo units like hotel rooms. Marriott has also capitalized on this opportunity by introducing its sub-brand Homes & Villas, a vacation rental platform. For many investors, this short-term rental model can typically yield higher income due to higher daily rates and the ability to adjust prices in high versus low seasons. The distinctive implication for the housing market here is that this approach significantly impacts housing affordability and the availability of long-term rentals.

As investors realize they can generate higher incomes via a short-term rental model through platforms like Airbnb, they are more willing to pay a premium for properties that otherwise wouldn’t be profitable if leased out traditionally. In other words, if a homebuyer can rent out their unit on occasion at the additional monthly mortgage amount from the premium, the decision to pay more can be justified. For example, a homebuyer may consider paying $100,000 over the listing price if they can rent out their unit for a weekend per month at a rate of $600-$665 since this would be the monthly mortgage payments assuming 6-7% interest rates. While this method can make homeownership “more affordable,” the increased willingness to pay at a premium further drives up prices.

On the other hand, long-term rents will rise due to limited supply and increased competition when more traditional units get converted to short-term units. The implication of this offers an opportunity for investors looking to acquire or develop multifamily properties. From core to opportunistic multifamily investors, there is an opportunity to capitalize on the tight rental markets by attracting tenants who were forced out of long-term lease apartments that have since been converted to a short-term model.

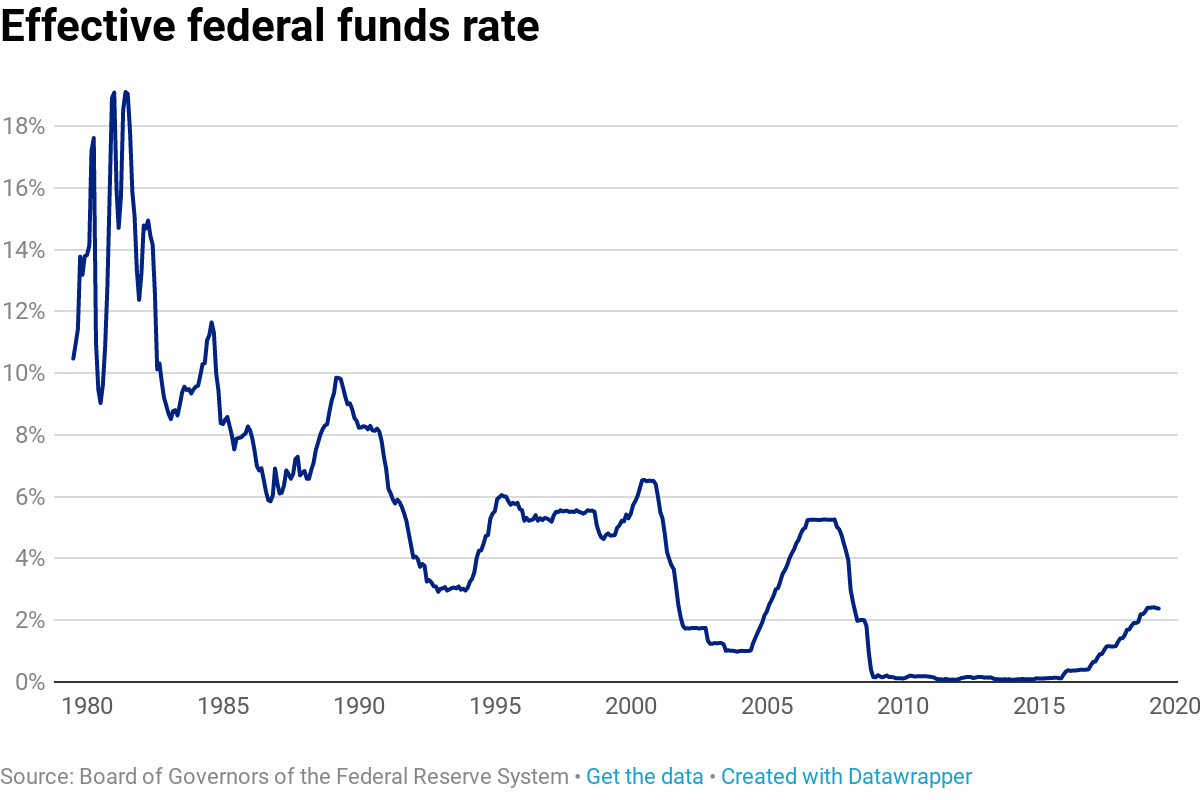

In the current economic environment, it’s critical to consider how the Fed’s interest rate hikes control rent price inflation and how that affects the housing landscape. Though the belief is that lowered consumer and business spending leads to lower home and rent prices, that might not be the case. Instead, rising rates can force frustrated buyers into the rental market, increasing competition. Also, rate hikes can limit new construction lending, reducing future housing supply. Either way, there is no clear correlation between rates and rents, but what’s clear is that such raises can create market instability and potentially force the economy into a recession. For short-term rental giant Airbnb, CFO Dave Stephenson says the possible economic downturn hasn’t been enough to cause concern as he believes the increasing number of tourists eager to get back to traveling can preserve demand even in tough economic times.(3)

The decline in homeownership among Millennials and their changing lifestyle preferences, combined with favorable industry trends and financial data, suggests that this short-term operating model is here to stay. Here at Lever Capital Partners, we pride ourselves on our ability to finance your next short-term rental project. Through our significant experience in the space, we are able to get you the most attractive financing the market has to offer. We look forward to discussing your next project and putting together a capital structure that best suits your needs.

References:

https://educationdata.org/student-loan-debt-by-generation

https://www.costar.com/article/1874040746/us-short-term-rental-market-poised-for-further-growth