What Rising Interest Rates mean for Commercial Real Estate

By: Daniel Li

2022 will be a transformative era for capital markets in all sectors of the U.S. economy. In order to combat inflation caused by the stimulus measures implemented by the Federal Reserve during the COVID-19 pandemic, the Federal Reserve has recently decided to accelerate plans to increase interest rates. On December 15th, 2021, the Federal Reserve announced that it would end its pandemic-era bond purchases in March of 2022 and plan for three 25 basis point interest rate hikes by the end of 2022.

Due to the leveraged nature of commercial real estate, the rate hike by the Federal Reserve will have significant impacts on both debt and equity markets. As properties are often financed with commercial mortgages, commercial real estate markets are most exposed to interest rate alterations. With the rise in interest rates, we see the cost of debt rising accordingly. There are many debates regarding whether there will be increases or decreases in cap rates as a result of the interest rate increase and current macroeconomic factors.

Fundamentally speaking, increased interest rates lead to more expensive financing. From an equity perspective, acquiring new properties will have narrower margins, and in turn, may create a more conservative market. From a debt perspective, the increased rates may cause a decline in deal flow, however that loss in volume may be balanced by increased margins on invested capital.

The record low federal fund rate at the beginning of the pandemic (0% to 0.25%) reduced the cost of financing, and as a result, instigated a surge in buy-side activity, development, and increased prices. As with any artificial injection of capital to stimulate the economy, there are repercussions; one of which being the rapid increase in inflation. Thus the Federal Reserve’s upcoming move to not only increase interest rates but to raise them ahead of schedule has been a long time coming.

To look at lasting effects on commercial real estate markets, lenders and investors are looking towards two factors regarding interest rates. One, the effect of the interest rate hikes on cap rates, and two, the adaptability of commercial debt markets in regards to a rate hike. Concerning cap rates, there are generally two ways they can move. One, many believe that a rise in interest rates correlates with a rise in cap rates as property values decrease. Two, others believe that with increased interest rates, investors pay more to borrow capital, cutting into profits, and thus decreasing cap rates. However, when considering cap rate movement in relation to interest rates, we must consider a longer timeframe. As a result, it becomes hard to predict changes in cap rates as a result of increased interest rates, as other factors come into play such as capital flows, investor sentiment, and real estate fundamentals. Historically, changes in federal interest rates have not resulted in immediate changes in cap rates. The ultimate question is whether the market is well prepared to adapt to such a change.

Broadly speaking, the effects of rising interest rates are unpredictable. In addition, recent geopolitical developments such as the Russia-Ukraine War make it uncertain where the Fed will go with interest rates. However, we are certain that they will go up, and as such, create an environment for the movement of cap rates and the exacerbation of current squeezes on markets.

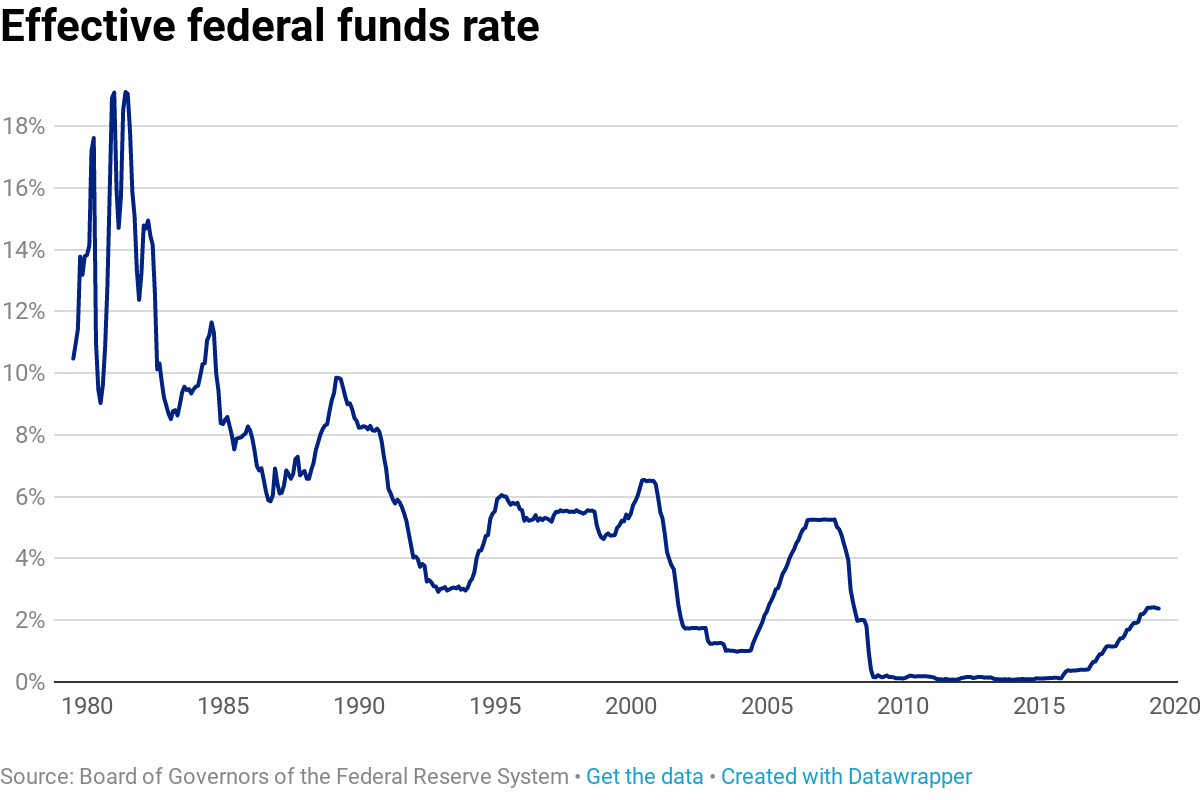

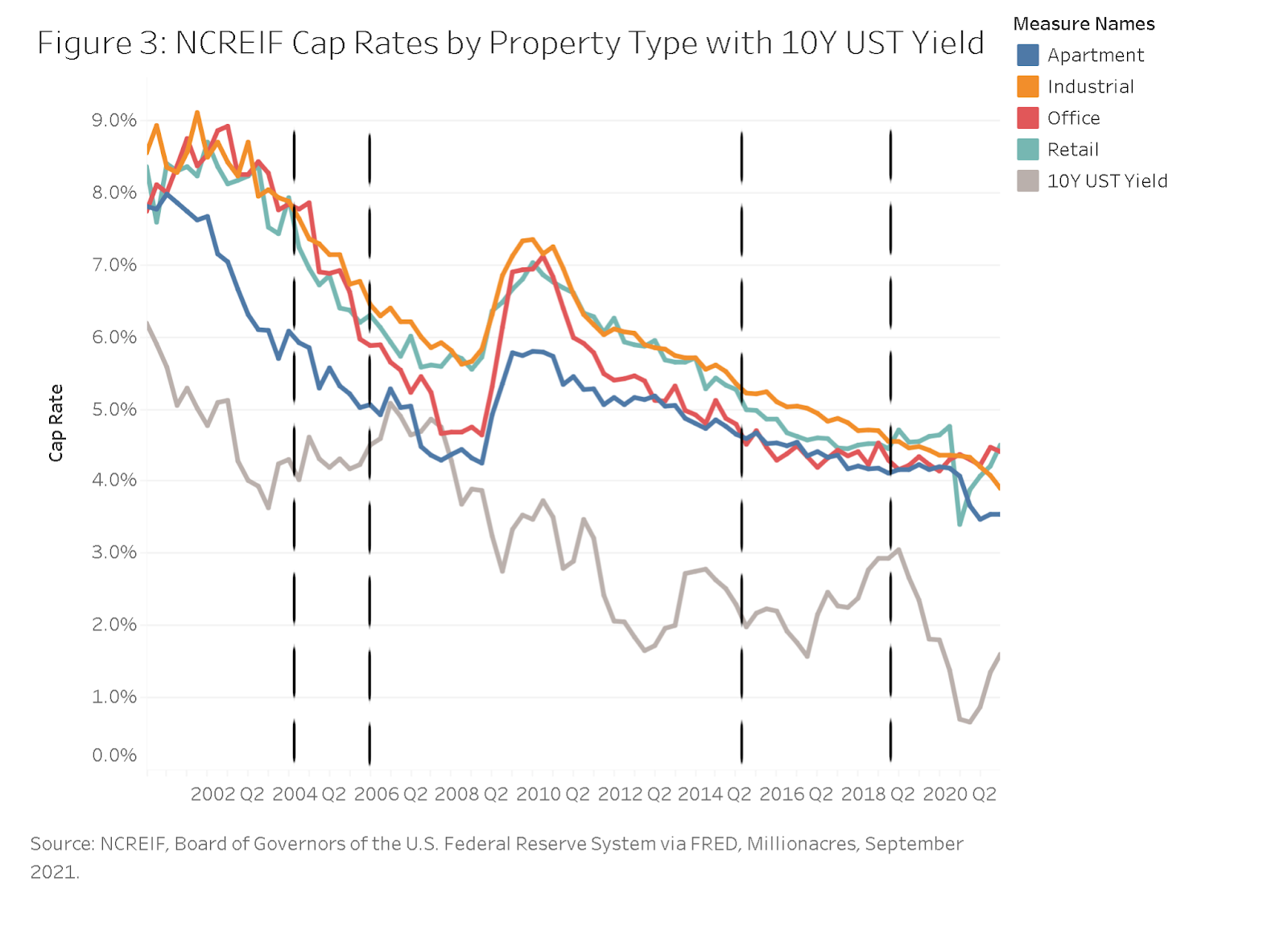

Graph 1.1

Graph 1.2

Secondly, we will see some asset classes take the hit worse than others. From the graphs above, we can see how historically speaking, with previous interest rate increases in 2015-2018 and 2004-2005, cap rates have generally compressed. However, stable cash-flowing asset classes with high occupancy rates such as multifamily will fare better than higher risk higher reward asset classes such as industrial, office, and retail. Since the margins on rent from these asset classes become tighter through the increase in interest rates, the risk of industrial, office and retail in regards to defaults will increase. We can see this through Graph 1.2, where apartment cap rates saw less compression than industrial, office, and retail asset classes. While the previous two interest rate hikes have led to cap rate compression, this is not indicative of what will occur in the present day. However, we do see that multifamily generally can withstand these macroeconomic trends better than office, industrial, and retail asset classes.

With the increase in the cost of financing, we will see spreads tighten as value add opportunities diminish. Since the market for many stable cash-flowing asset classes such as multifamily are already facing extreme demand and competition, the increasing cost of debt due to interest rate hikes will continue to chip away at the returns of value-add opportunities. According to Forbes, many investors in 2020 faced a difficult decision of either accepting lower returns with the appropriate amount of risk or finding ways to add more value to hit more opportunistic returns. The interest rate hikes of 2022 will exacerbate this trend as financing becomes more expensive. Ultimately, the interest rate hike will make competitive markets less viable, pushing investors to do two things. One, more conservative strategies such as core and core-plus will be adopted in order to accommodate for the increasing competitiveness of value-add opportunities, and two, we will see expansion towards suburban areas. Regions such as many of the Sun Belt states (i.e. Texas, North and South Carolina, and Florida) have high suburban demand for multifamily. According to Matthews Real Estate Investment Services, the demand in this region is driven by rapid population growth and increasing employment opportunities. With these growth and demand drivers, investors are looking to those areas to find more lucrative value-add opportunities.

According to Cushman and Wakefield, in the long term, this rate increase will benefit the health of property markets. The purpose is ultimately to reduce the potential for inflation to become entrenched, giving way to a more aggressive hike in the future, and potentially causing a recession. In the short term, interest rates are not necessarily a shift away from the current norm, but a force that can exaggerate many of the effects we saw in recent years. Multifamily will continue to offer stable returns, despite its slow yet steady cap rate compression, and investors will become more risk-averse and/or find opportunities in emerging markets.

In a constantly changing market, one slow step could be a missed opportunity. At Lever Capital Partners, our steadfast team of industry experts track the latest trends and understand how to source and utilize the best available capital. Whether you are looking for an equity partner, a lender, or a combination to fund your next project, Lever can advise you on obtaining the most attractive financing the market has to offer. Here at Lever Capital Partners, we pride ourselves on our wide range of experience in refinancing, recapitalizing, converting assets, ground-up construction, acquisitions, and our overall creativity in getting our clients the capital they need for any commercial real estate related transaction. Our industry professionals look forward to speaking with you about your next project.

References:

https://www.federalreserve.gov/monetarypolicy/openmarket.htm