From Crisis to Opportunity: Investing in the Rebounding Hospitality Industry

by: Ethan Ritz

The emergence of COVID-19 and the pandemic that followed created a ripple effect that impacted nearly all industries in the economy, specifically hospitality. 2020 represented the worst year in recorded history for United States hospitality with unsold rooms per night reaching an excess of one billion dollars surpassing the prior peak of 786 million during the 2009 recession (1). While the economic consequences of the pandemic still linger, the hotel industry is steadily making a comeback. Three years removed from 2020, with the demand for travel increasing rapidly and a surge in hotel construction projects ensuing, hospitality investment has become a bullish investment choice.

In the United States, hospitality performance has already exceeded the levels attained prior to the pandemic. According to the U.S. Travel Association, travel spending totaled $93 billion in February 2023 which is 5% above the levels earned in 2019 (2). Furthermore, since July 2021, average daily room rates surpassed comparable 2019 levels in every month but one (January 2022 missed by $0.35) (3). This drastic change is directly correlated to the sharp increase in the demand for travel. In a study by Destination Analysis that involved 4,000 Americans answering about their budget prioritization, domestic leisure travel took the top spot, with 35% of American travelers saying that it will be a high or extremely high priority in their household spending this year. This beat out restaurants (32%), education (24%), home improvement (21%), clothing & accessories (20%) and entertainment (18%) (4). In addition, a study by Oxford Economics stated that 89% of global business travelers wanted to add a private holiday to their business trips in the next twelve months (5). It is clear that regardless of the type of traveler, the demand for travel has significantly risen and become a priority purchase for a large portion of Americans. Due to this, current investment in the hospitality industry when prices are still low could prove bountiful.

As demand for travel continues to rise, the construction of the hotels used to host these eager travelers has also moved in a similar direction. At the end of 2022’s fourth quarter, the U.S. construction pipeline was up 14% by projects and 12% by rooms year-over-year, according to Lodging Econometrics. 2022 saw new project announcements up 35% year-over-year and construction start-ups increasing by 36% year-on-year (6). In particular, two cities, Dallas and Atlanta, which have become two of the hottest spots for investment, are leading the way in hotel construction. At the end of the fourth quarter of 2022, Dallas had 176 projects with 20,790 rooms and Atlanta had 145 projects with 18,100 rooms (6). In terms of hotel developers, the Marriott, Hilton, and Intercontinental groups were the three largest companies in the fourth quarter of 2022 in terms of projects and rooms with the Marriott constructing 1,490 projects with 180,113 rooms, the Hilton constructing 1,378 projects with 154,790 rooms, and Intercontinental constructing 789 projects with 78,951 rooms (6). Given these key performance indicators from the fourth quarter of 2022, for investors interested in the hospitality industry, equity should be considered for allocation in Dallas and Atlanta under projects managed by the Marriott, Hilton, and Intercontinental. Furthermore, hospitality construction has been thriving throughout the U.S. under a variety of developers, so any investment nationwide in this industry is likely to be successful.

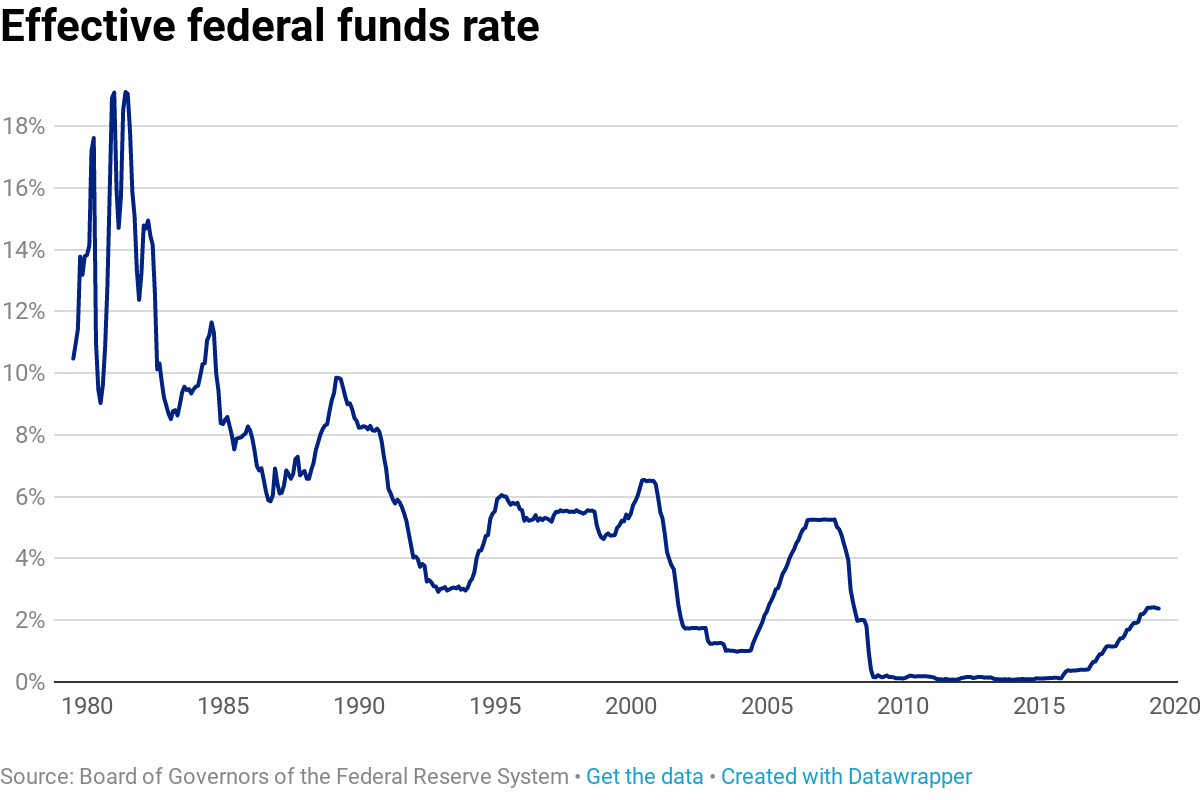

However, in spite of these positive trends for hospitality investment, the industry is also facing increased speculation due to rising interest rates and the recent collapse of SVB bank. The federal funds rate currently sits at 4.83%, which is significantly higher than the rate of .33% from a year ago today (7). As the interest rate continues to rise, investors have begun focusing less on hospitality investment due to its growing costs. In addition, the recent collapse of SVB bank has caused uncertainty within the industry, as the bank was a major player in financing hotel projects with over $2.6 billion dollars worth of loans in commercial real estate (8). This has led to banks becoming warier to lend money into hospitality and to increased caution from potential investors. Unless the Fed gradually decreases its rate, there is the potential for a halt in hospitality construction. In turn, this potential halt in construction could create an undesirable market space for investors. As such, while the hospitality industry still remains an attractive option for investors, caution should also be taken given these recent events.

Investment in hospitality will always remain a high-risk, high-reward decision. The end of the pandemic represents a time period where that level of reward has never looked more appealing. Even with rising interest rates and the SVB bank collapse, due to the pent-up demand for travel and the rise in new hotel constructions, the hospitality industry is poised for a breakthrough in profitability.

References: